Why did the USDBRL rise so much in 2024?

Dollar’s global strength

During the Covid-19 pandemic, the imbalance between heated demand due to fiscal and monetary stimuli and supply capacity limitations resulted in the acceleration of inflation indices in several nations. Facing the inflationary challenge, the central banks of the main economies gradually raised their basic interest rates to significantly tighten financial market conditions and stabilize price levels. This movement occurred in an uncoordinated manner among monetary authorities, led by the Federal Reserve (Fed) —the central bank of the United States— which implemented the fastest and most rigorous monetary tightening in the last four decades.

The rise in American interest rates further increased the attractiveness of bonds from the world's main financial center and issuer of the most used currency in economic transactions between countries. Thus, in addition to being considered a safe haven during moments of turbulence and stress in the global financial system, US bonds now offer the highest yield among advanced economies, boosting the demand for the currency and appreciating it against other currencies.

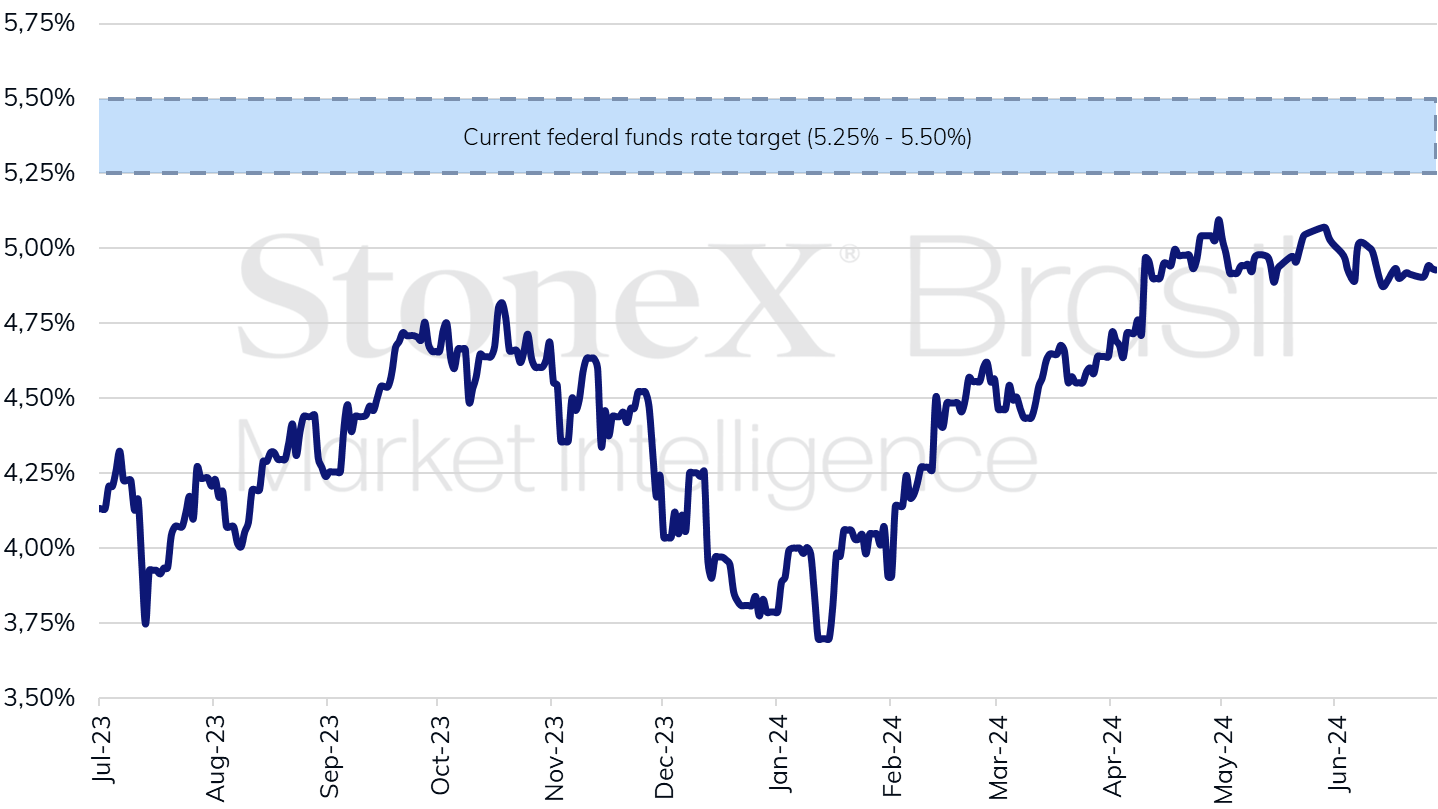

The outlook for the coming months still favors a strong dollar, as investors have progressively reduced their bets on rate cuts by the Fed after several consecutive months of stronger-than-expected economic performance and unexpected inflation persistence in the US in the first quarter of 2024. Additionally, the institution itself has indicated in its monetary policy decisions that it intends to be cautious with reductions in its basic interest rate, aiming to ensure that the country's inflation returns to the desired 2% annual target safely and sustainably. Thus, the chart below shows that since April, investors have been betting on only two rate cuts by the Fed in 2024, ending the year in the range of 4.75% to 5.00% p.a.

Weighted average of bets between July 2023 and June 2024 for the level of the American federal interest rate at the end of this year.

Source: CME FedWatch Tool. Design: StoneX. Refers to the average daily bets in the futures interest market on the indicated date, weighted by their probabilities.

In addition to the attractiveness of higher yields from low-risk bonds, higher economic growth among major economies contributes to the increased attraction of productive and financial investments worldwide. Indeed, the IMF estimated this year that one-third of global financial flows between 2020 and 2023 were directed to the United States, compared to an average participation of 18% between 2010 and 2019, highlighting the strong demand for U.S. assets by global investors. Conversely, this scenario reduced investors' appetite for risky assets such as stocks, commodities, and currencies of emerging countries.

Confidence Crisis in Brazil

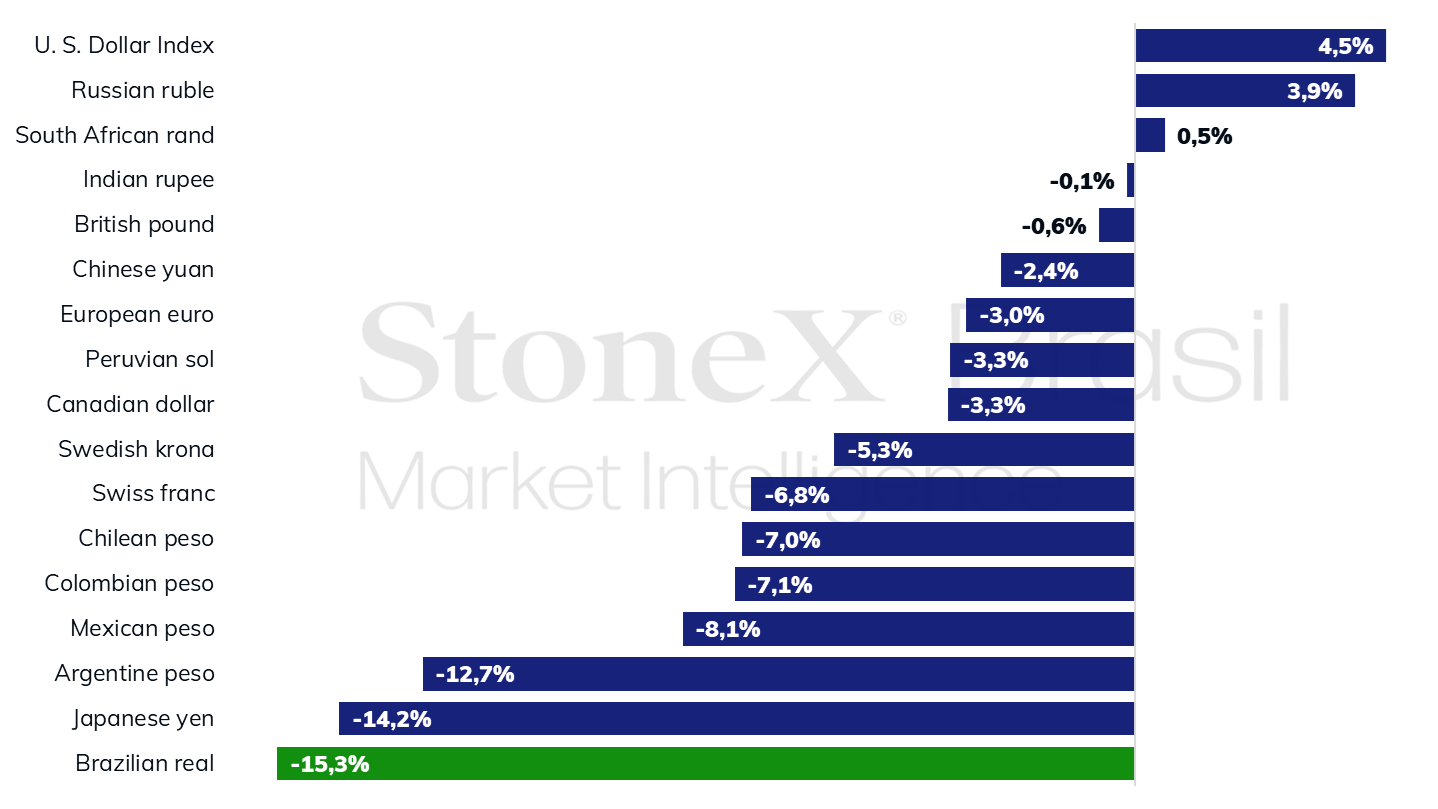

Although the moment is one of global dollar strength, the Brazilian real depreciated significantly more than its peers in the first half of the year, driven by a confidence crisis among investors regarding the conduct of fiscal and monetary policies in Brazil. The loss of credibility began when the federal government decided to relax budget targets for 2025 and 2026 by submitting the 2025 Budget Guidelines Bill to the National Congress on April 15. These changes occurred just a year after the presentation of the new fiscal framework bill, initiating a process of raising inflation expectations for Brazil. Subsequently, the divided decision on May 8 by the Central Bank's Monetary Policy Committee (Copom), where the four members appointed by President Luiz Inácio Lula da Silva voted for a higher rate cut and the five members appointed by former President Jair Bolsonaro voted for a smaller cut, generated concern among investors that Copom's stance would become more tolerant of inflation from 2025 onwards when there will be a majority of members appointed by the current government. Consequently, inflation expectations continued to rise, and the credibility of economic policies diminished.

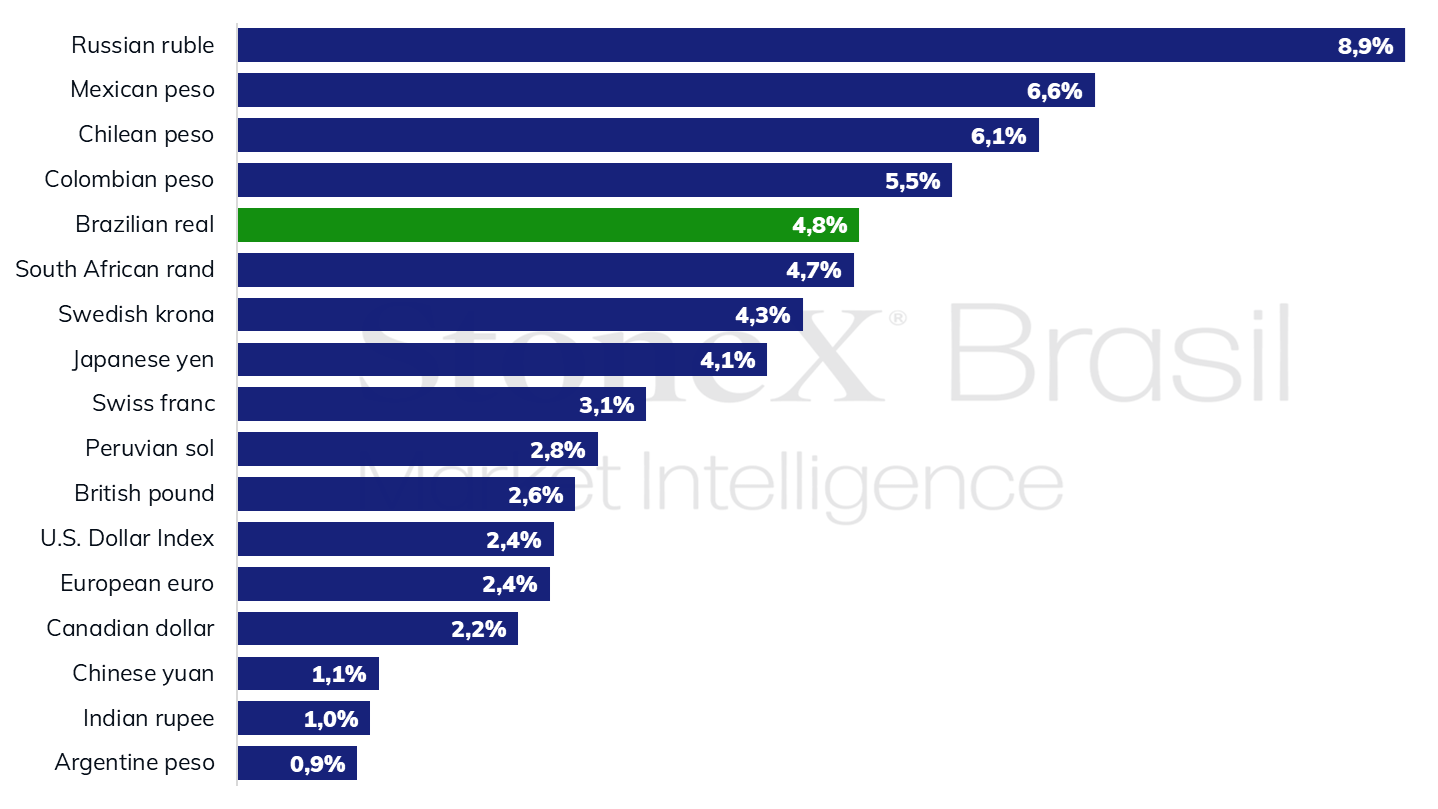

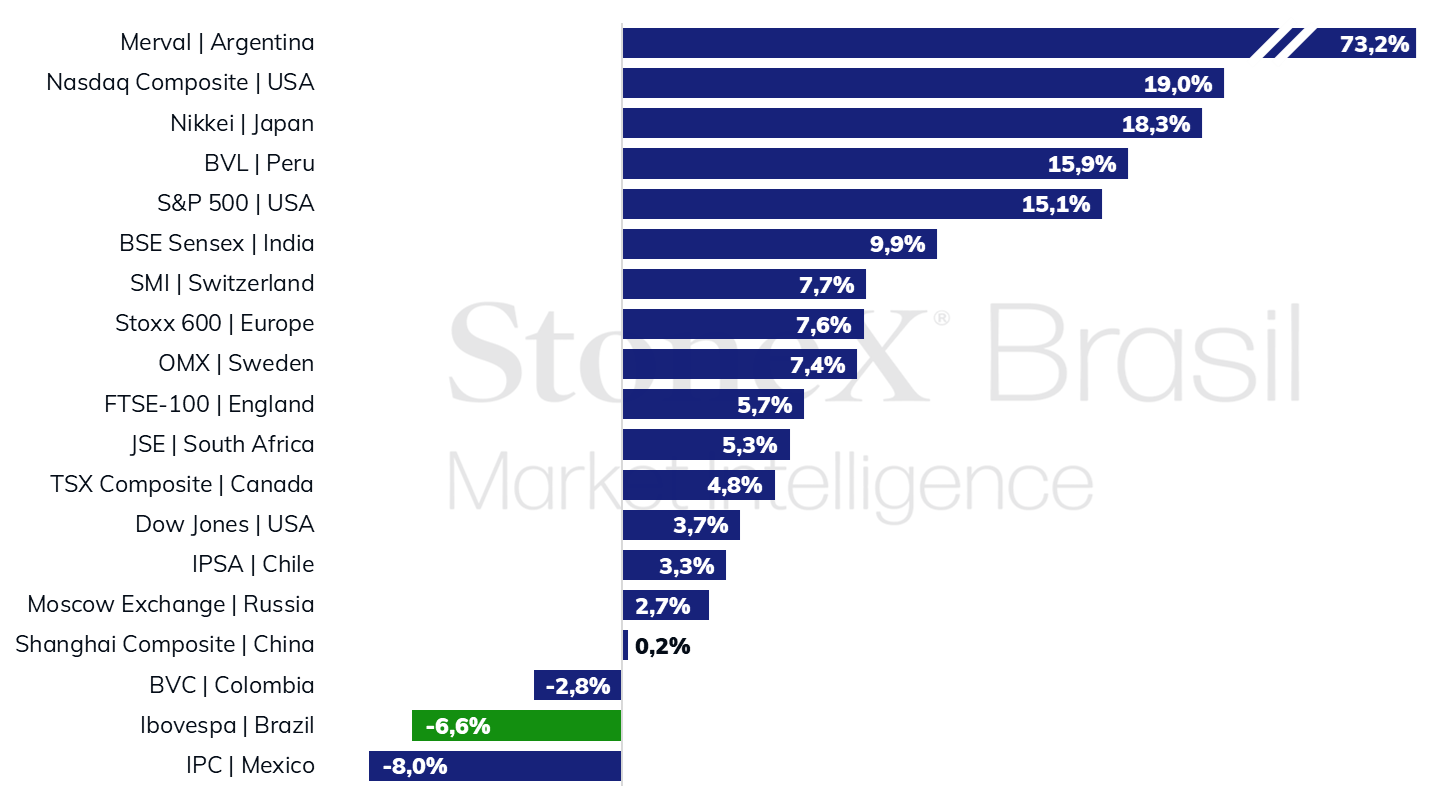

The trend of pessimism and risk perception for Brazilian assets was deepened by repeated criticisms from President Lula of both the monetary policy and the Central Bank president, Roberto Campos Neto, as well as comments downplaying the need for public spending adjustments. These statements reinforced the financial market's concern about the sustainability of public debt, the federal budget balance, and the Central Bank's autonomy. As a result, the currency, stock market, 10-year interest rates, and the requirement for premiums for Brazil's 5-year Credit Default Swaps (CDS) in the first half of 2024 were among the worst performers compared to relevant central and emerging economies.

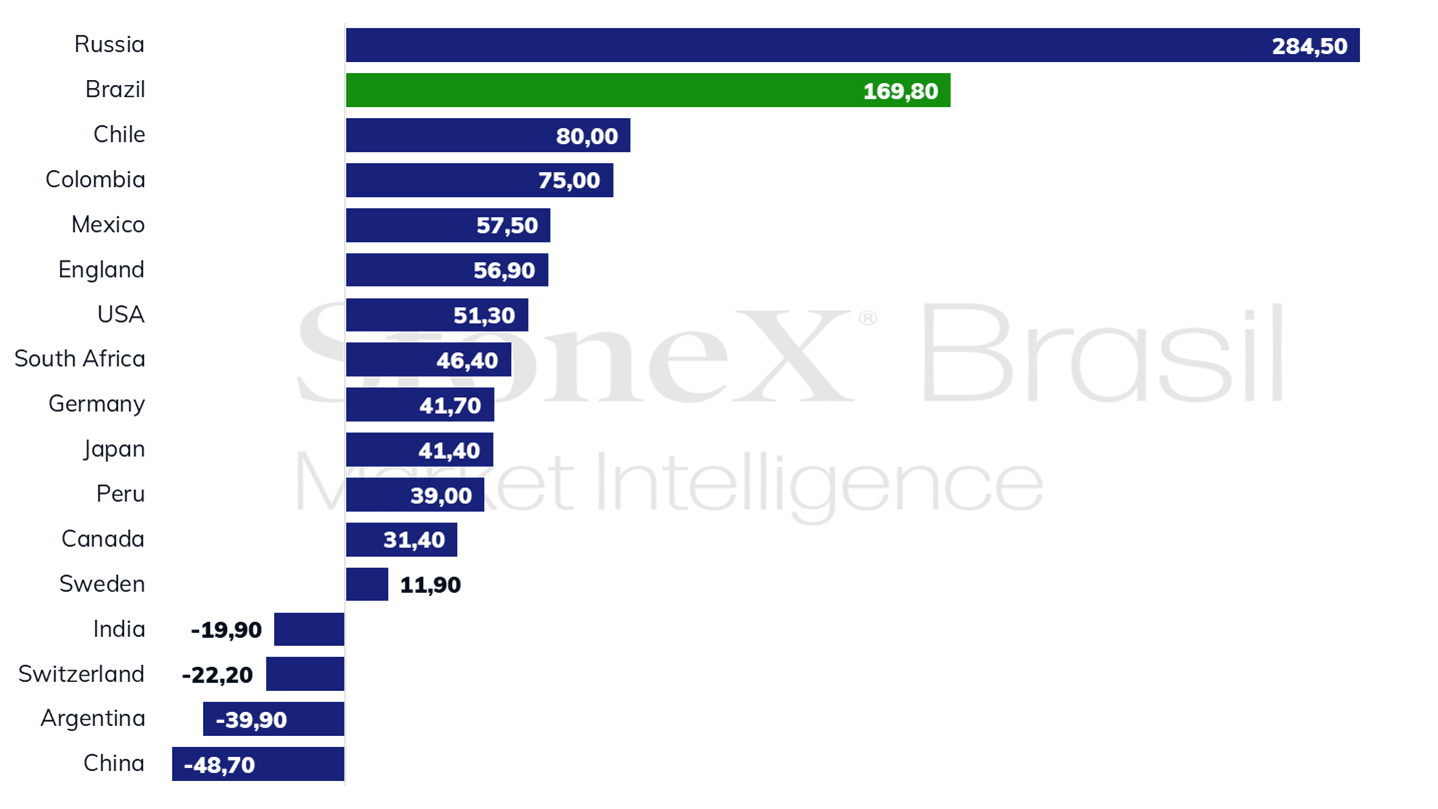

Variation of selected currencies against the dollar in the first half of 2024 (%)

Sources: Refinitiv and Bloomberg. Design: StoneX.

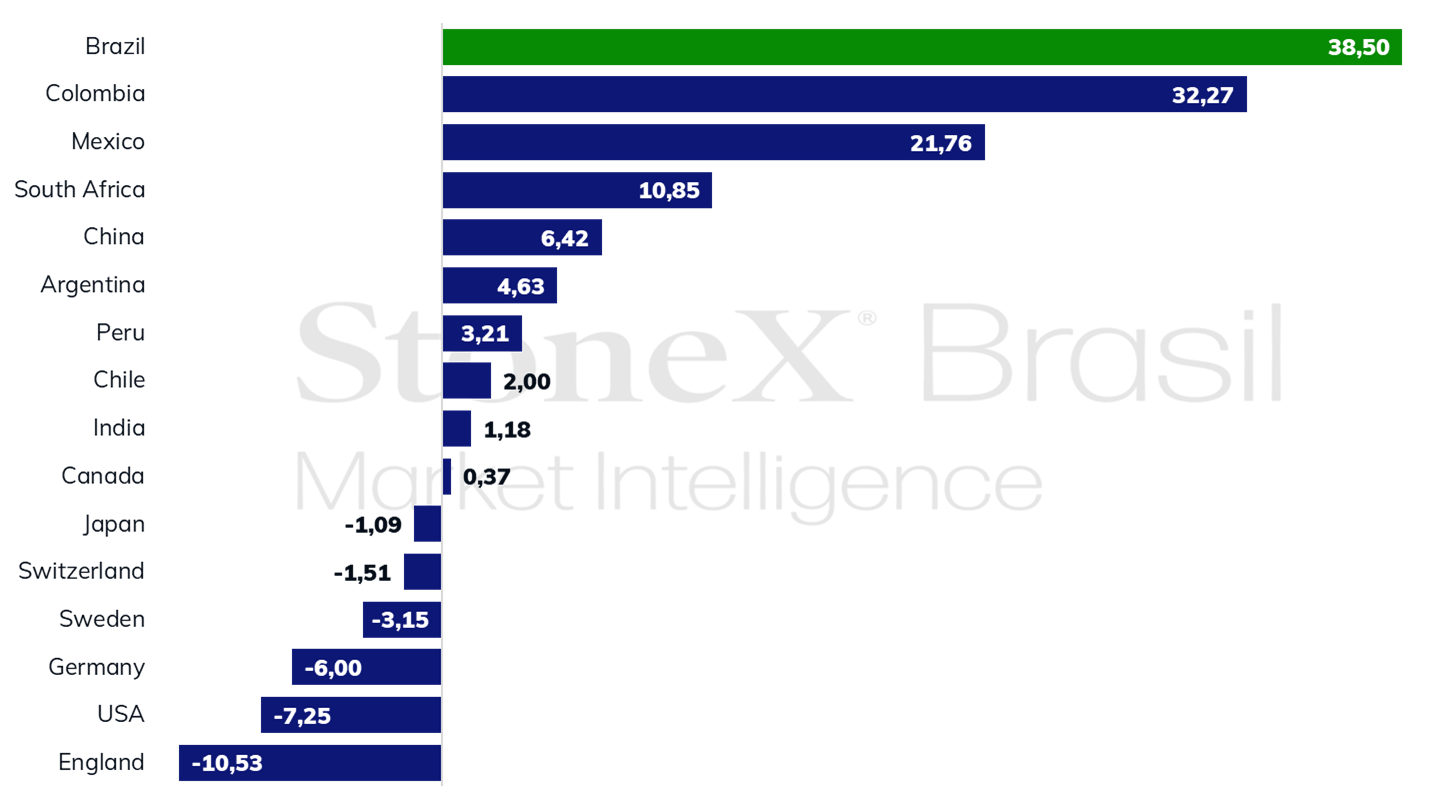

Volatility of selected currencies in the first half of 2024 (%)

Sources: Refinitiv and Bloomberg. Design: StoneX.

Variation of selected stock indices in the first half of 2024 (%)

Sources: Refinitiv and Bloomberg. Design: StoneX.

Variation of 10-year bond yields in selected countries in the first half of 2024 (basis points)

Sources: Refinitiv and Bloomberg. Design: StoneX.

Variation of 5-year Credit Default Swaps (CDS) in selected countries in the first half of 2024 (basis points)

Sources: Refinitiv and Bloomberg. Design: StoneX.

Note: basis point = 0.01 percentage point.

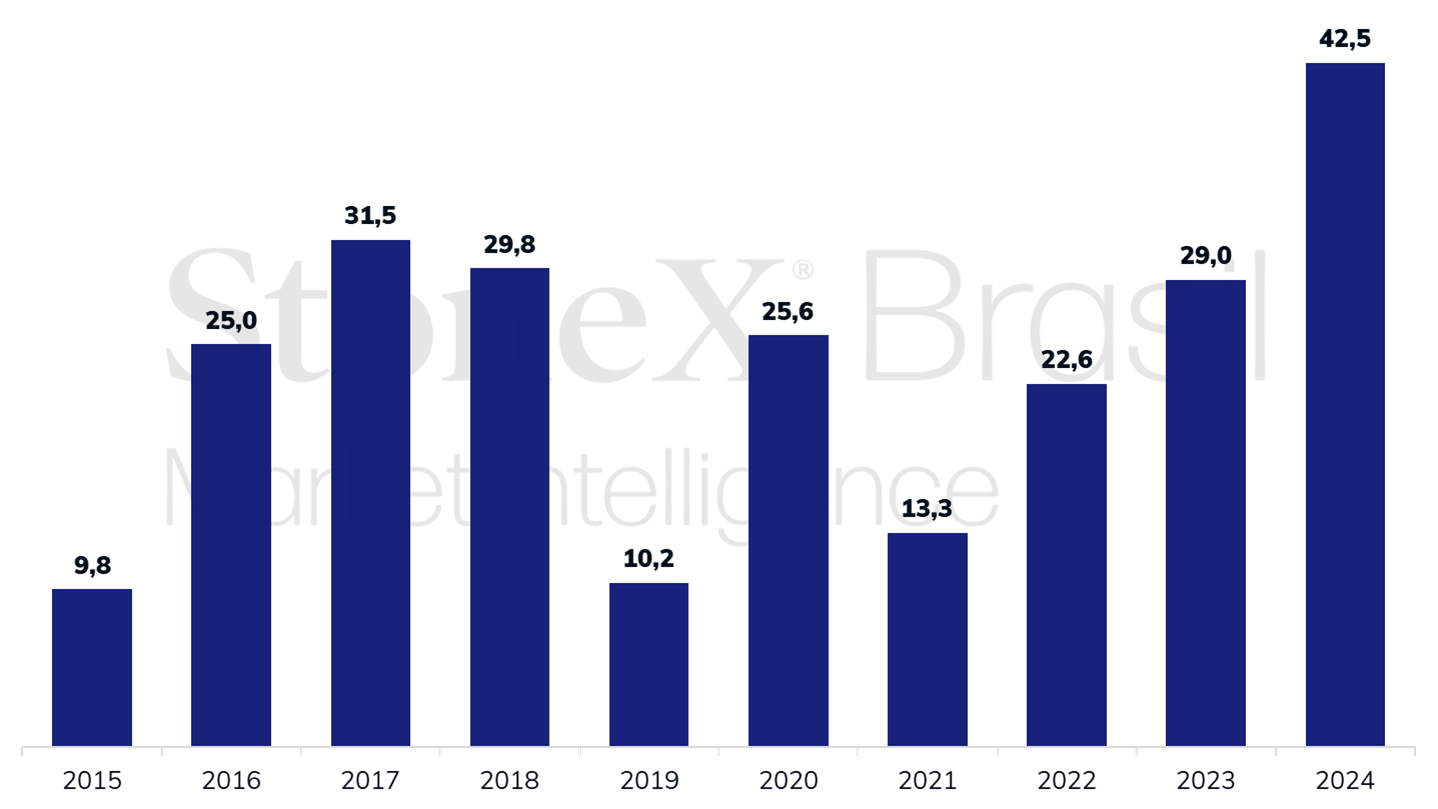

This negative performance of the Brazilian currency seems largely disconnected from the fundamentals of external accounts, given that the trade flow surplus in the first half of 2024, of US$ 42.5 billion, was the highest for the period since 2007 (US$ 45.9 billion), while the deficit of the "financial" flow (including movement of services, income, and capital) in this period is significant, at -US$ 30.6 billion, but still far from the record US$ 38.1 billion in 2020. Thus, the positive balance of US$ 11.9 billion for the year would be more compatible with a strengthening real, not with a 15.3% weakening.

Foreign exchange flow - Cumulative balance of the trade account in the first half of the year (US$ billion)

Source: Central Bank of Brazil. Design: StoneX.

Foreign exchange flow - Cumulative balance of the financial account in the first half of the year (US$ billion)

Source: Central Bank of Brazil. Design: StoneX.

Thus, the negative performance of Brazilian assets and the worsening expectations for the country's macroeconomic variables are likely to prevail in the short term unless the federal government demonstrates concrete actions to sustain the Central Bank's autonomy and the rigidity of the fiscal framework, particularly with measures for federal spending adjustments.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights