Escalation risk in the Gulf remains elevated after reports of explosions near Iran’s Qeshm Island and alleged Iranian missile/drone retaliation against U.S.-linked targets across Kuwait, Bahrain, and regional waters. The IRGC claimed it struck U.S. bases and the 5th Fleet headquarters, while CENTCOM denied those claims and said U.S. forces defeated Iranian missiles and drones, including attacks aimed at civilian maritime traffic. The most market-sensitive developments are the reported mining of parts of the Strait of Hormuz, U.S. self-defense strikes on Qeshm Island, and the disabling of a tanker headed toward Iran, all of which raise the risk premium for crude, shipping, insurance, and broader commodity markets. At the same time, diplomatic channels appear to remain open, with Trump pushing Iran for written nuclear commitments and regional intermediaries reportedly working to prevent a wider escalation, suggesting the situation is dangerous but not yet fully out of diplomatic control.

USTR’s Section 301 findings broaden the trade-policy risk map by targeting 60 economies for alleged failures to address forced-labor goods in trade flows, including major U.S. partners such as China, India, Japan, the UK, EU, Mexico, Canada, and Australia. The proposed actions suggest Washington is moving beyond country-specific tariff disputes toward a wider enforcement framework tied to labor standards and supply-chain compliance. For markets, this adds another layer of uncertainty around import costs, retaliation risk, and future trade negotiations, especially because several of the named economies are also key buyers or suppliers in agriculture, manufacturing, energy, and consumer goods. The immediate impact may be limited until specific tariff or enforcement measures are finalized, but the headline reinforces that trade policy remains a major source of volatility.

According to the Wall Street Journal, the U.S. Deputy Agriculture Secretary said China has started placing orders for soybeans currently being planted across the U.S. That is a supportive signal for new-crop soybean demand, as it suggests China may be preparing to re-engage the U.S. export program for fall shipment rather than relying only on Brazil. The headline helps ease concerns that China would stay heavily concentrated on South American supplies, but the market will still need to see confirmed sales volumes, shipment timing, and sustained follow-through before making a bigger balance-sheet adjustment. For now, it is a friendly soybean-market development, but not yet a demand game-changer unless the orders build consistently.

Mexico’s recommendation to extend the USMCA agreement for 16 years is a constructive signal for North American trade stability, especially as the U.S., Mexico, and Canada move through review discussions. A longer extension would reduce uncertainty for businesses that depend on cross-border supply chains, including agriculture, autos, energy, livestock, food processing, and manufacturing. For U.S. agriculture, the headline is generally supportive because Mexico remains a key buyer of U.S. corn, soy products, meat, dairy, and other farm goods. That said, the extension would still need agreement from all three countries, and unresolved issues around tariffs, autos, labor, biotech corn, steel, aluminum, and softwood lumber could still complicate negotiations.

Canadian Minister Responsible for Canada-U.S. Trade Dominic LeBlanc said he had a positive meeting with USTR Jamieson Greer, while raising Canada’s concerns over U.S. tariffs on autos, steel, aluminum, and softwood lumber. The tone sounds constructive, but the substance shows major trade frictions remain unresolved ahead of continued talks. LeBlanc’s plan to stay in contact with Greer next week, along with bilateral discussions with Mexico on the USMCA, suggests Canada is trying to keep negotiations active and coordinated while pushing back on sector-specific tariff pressure. For markets, this keeps North American trade policy risk alive, particularly for autos, metals, lumber, manufacturing inputs, and cross-border ag supply chains.

White House economic adviser Kevin Hassett said gasoline prices are expected to move lower as the U.S. receives additional oil supplies from the Gulf, reinforcing the administration’s effort to ease fuel-price pressure. Separately, the White House is reportedly considering a plan to offer discounts on oil drilling licenses or fees on military and public lands in exchange for producers sending a share of the oil they drill into the Strategic Petroleum Reserve. The proposal is not finalized, but it suggests the administration is looking for ways to both encourage domestic production and rebuild the SPR without relying only on direct government purchases. For markets, the headline is modestly bearish for gasoline and crude sentiment if additional supply materializes, while also supportive of longer-term U.S. energy-security policy.

The U.S. Appeals Trade Court order for broad IEEPA tariff refunds is a potentially significant cash-flow positive for importers, but the issue remains tied up in appeals and legal uncertainty. If upheld, the ruling could force CBP to return large amounts of tariff payments collected under IEEPA authorities, benefiting companies exposed to imported inputs, retail goods, machinery, autos, and some ag-related supply chains. However, because the administration is appealing, the timing, scope, and eligibility for refunds remain unclear, and broader tariff risk is not going away as the White House continues to use other trade tools.

China’s RatingDog Services PMI came in much stronger than expected at 54.4 in May versus 52.3 expected and 52.6 previously, while the Composite PMI improved to 54.0 from 53.1. The data points to a firmer services-led recovery and suggests domestic activity had better momentum than expected in May. For markets, this is mildly supportive for risk sentiment and commodity demand expectations, especially if stronger services activity feeds into broader consumer spending and business confidence. That said, the improvement is more clearly tied to services than manufacturing, so the read-through to bulk commodities and industrial demand is supportive but not outright bullish by itself.

India’s statement that it remains in talks with the U.S. suggests New Delhi is trying to keep negotiations open and avoid a broader trade escalation after Washington proposed fresh tariffs on major trading partners. The headline is constructive in tone, but it also confirms that tariff risk remains active across key global supply chains. For markets, the main focus will be whether India can secure exemptions, delays, or a negotiated framework that limits the impact on goods trade. Agriculture, energy, pharmaceuticals, technology, textiles, and manufacturing inputs could all remain sensitive until there is more clarity on the final tariff structure.

Fed Chair Kevin Warsh is signaling an early focus on institutional reform while trying to reassure staff that changes will preserve the Fed’s core traditions and credibility. His memo points to a “clear-eyed” review process, suggesting potential changes in how the central bank operates, communicates, or structures policy advice without framing it as a break from the Fed’s mission. The decision to bring in outside advisers Paul Winfree and Daniel Heil, according to the Wall Street Journal, reinforces that Warsh is moving quickly to shape his leadership team and policy agenda. For markets, the key takeaway is that Fed reform is becoming an active theme, but Warsh appears to be balancing that with an effort to maintain continuity and institutional confidence.

Overnight options activity

Corn

B 500 z 440/400 ps 9 7/8 to 10

S 100 u 450 p 21 1/8

B 500 q 470 c 9 1/8

S 150 h 500 c vs b h 455 p 5 cr

B 1000 sd n 490 c 2 5/8

S 200 z 510/485 ps 18 ½ to 18 3/8

B 600 n 435 c 10 7/8

Beans

B 600 n 1240 c 1 ¼ to 1 3/8

B 500 n 1200 c 5 1/8 to 5 3/8

B 150 x 980 p 2

B 1250 x 900 p 3/4

B 500 n 1130/1110 ps 2 1/4

Bean oil

S 500 z 84 c 1.780 to 1.770

B 100 n 7750 c vs s 200 n 80 c .160 cr

B 100 n 70 p .100

Wheat

B 350 n 680 p 64 3/8

B 200 u 800 c 3 1/4

Open interest changes

corn

March 520/560 call spread buy, march 530/630 call spread buy, july 410 put buy and dec 500 call buys were new....march 650 call buy, short july 500 call buy, aug 505 call buy, dec 600 call buy and july 500 call sales were closing....short aug 480/500 call spread buy and sept 500/550 call spread buys were rolling longs.

Beans

Nov 1280/1380 call spread buy, july 1140 put buy and july 1180 call buys were new. Short july 1220 call buys were closing...nov 1150/1120 put spread sale and nov 1150/1100 put spread sales were closing.

Bean oil

Aug 73/68 put spread buy and july 75 put buys were new

Wheat

July 580 put buys were new

Kc wheat

July 750 call buy was closing

Lean hogs

Aug 102 call buy was new

Live cattle

June 248 put buy was closing...oct 240 call buy was new

Cvol

Ags 19.37% up .06%

Corn 23.01% down .07%

Beans 14.37% up .28%

Soymeal 18.27% down .38%

Bean oil 24.64% down .31%

Wheat 27.47% down .61%

Feeder cattle 16.34% up .08%

Live cattle 15.86% up .44%

Lean hogs 23.28% up .10%

Class 3 milk 20.26% up .24%

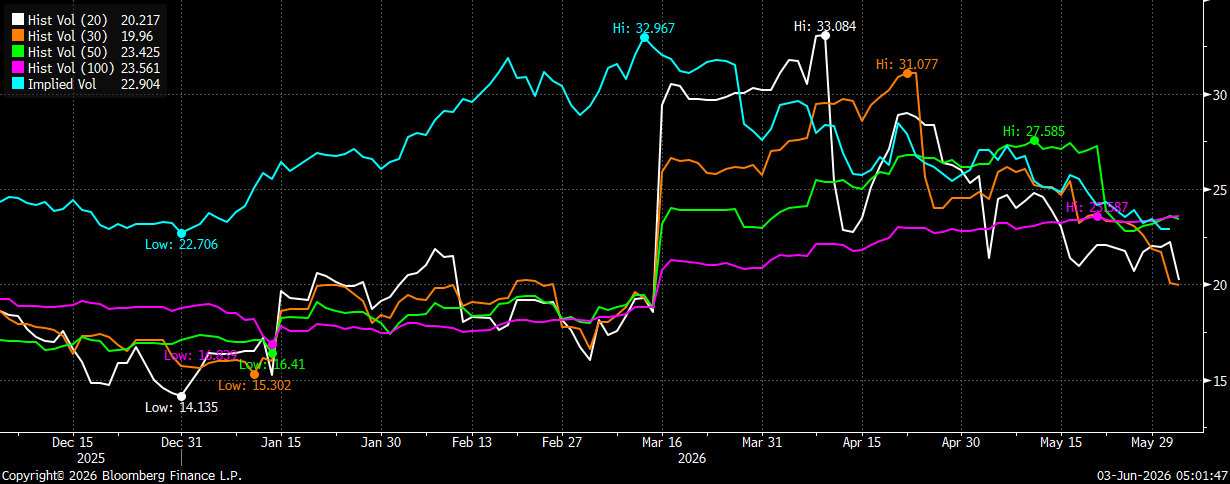

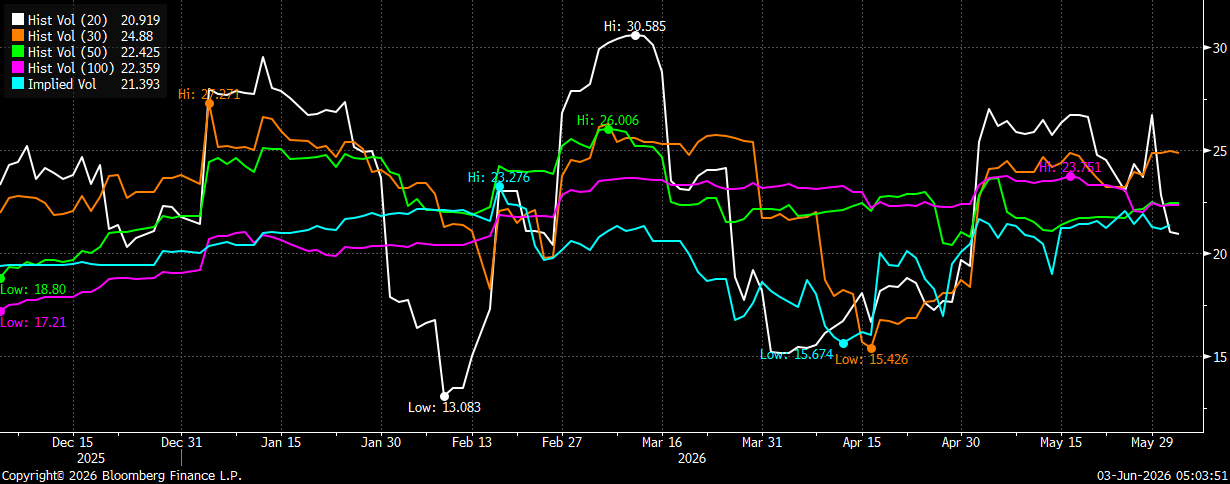

Corn (z)

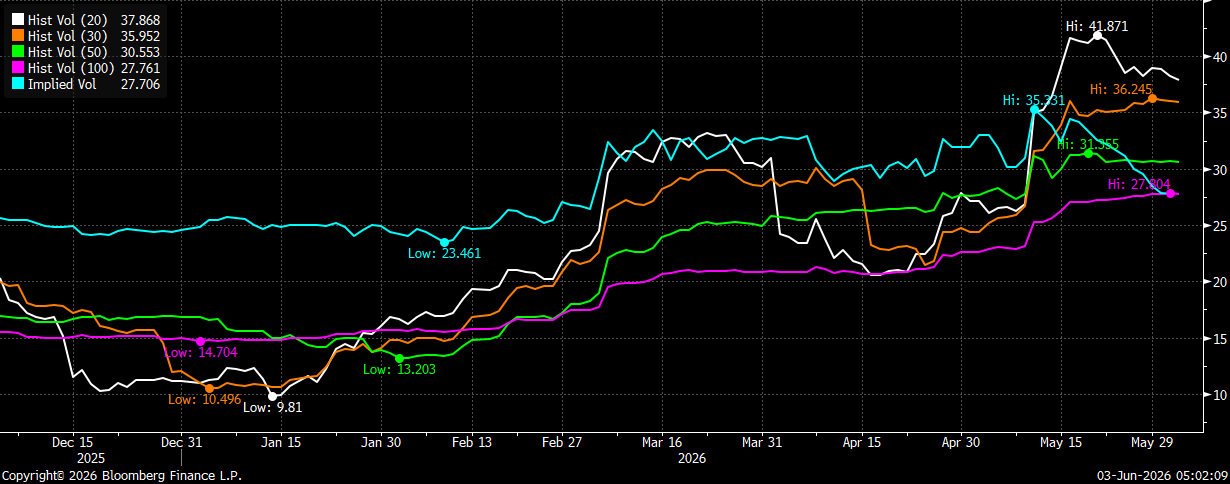

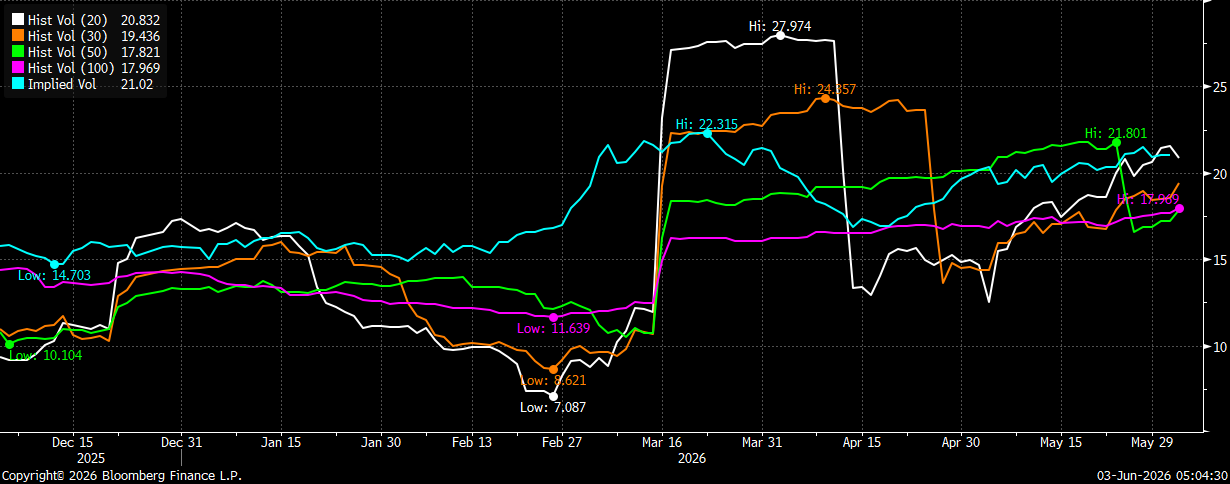

Beans (x)

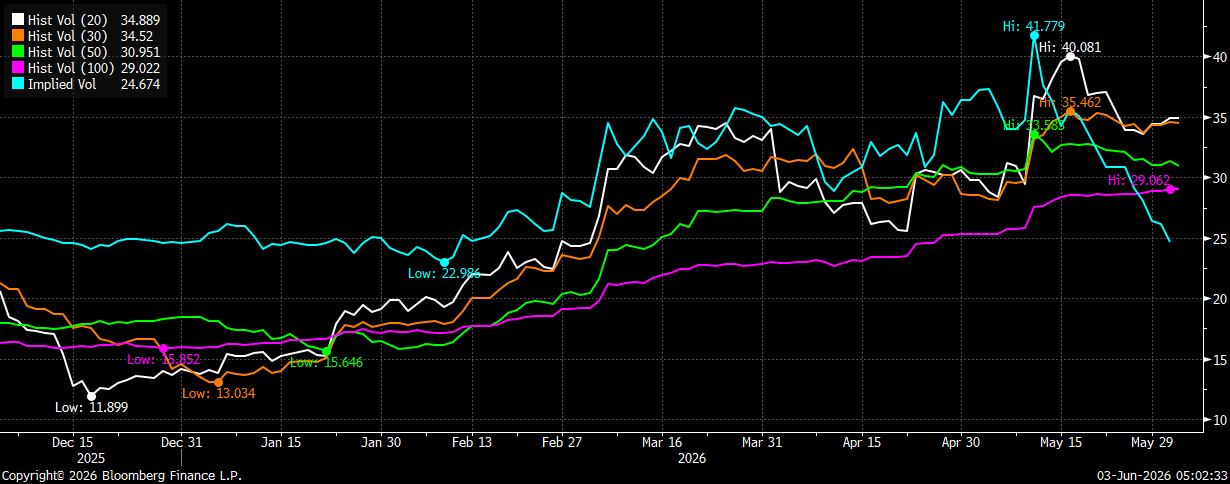

Soymeal

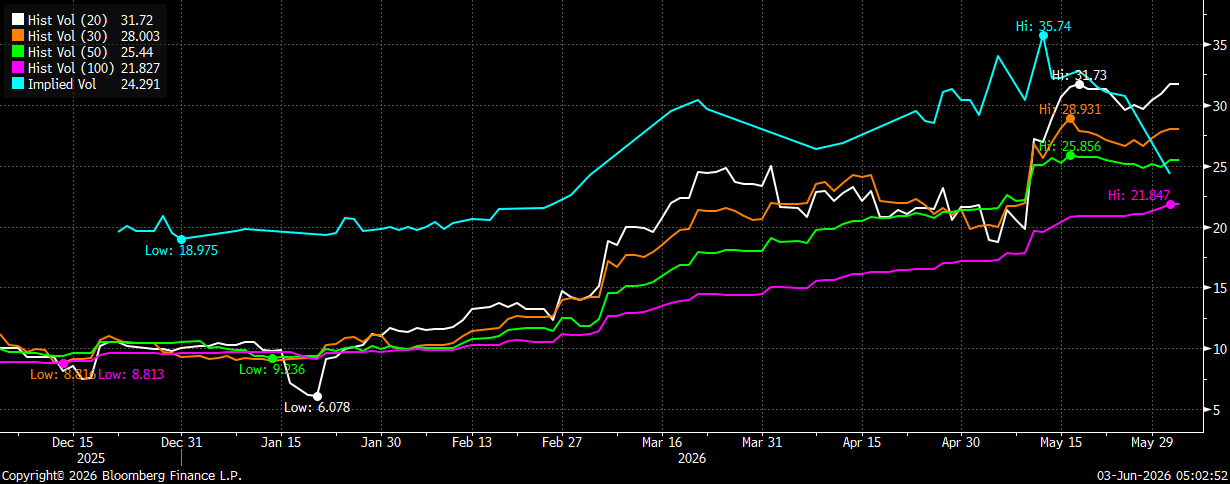

Bean oil

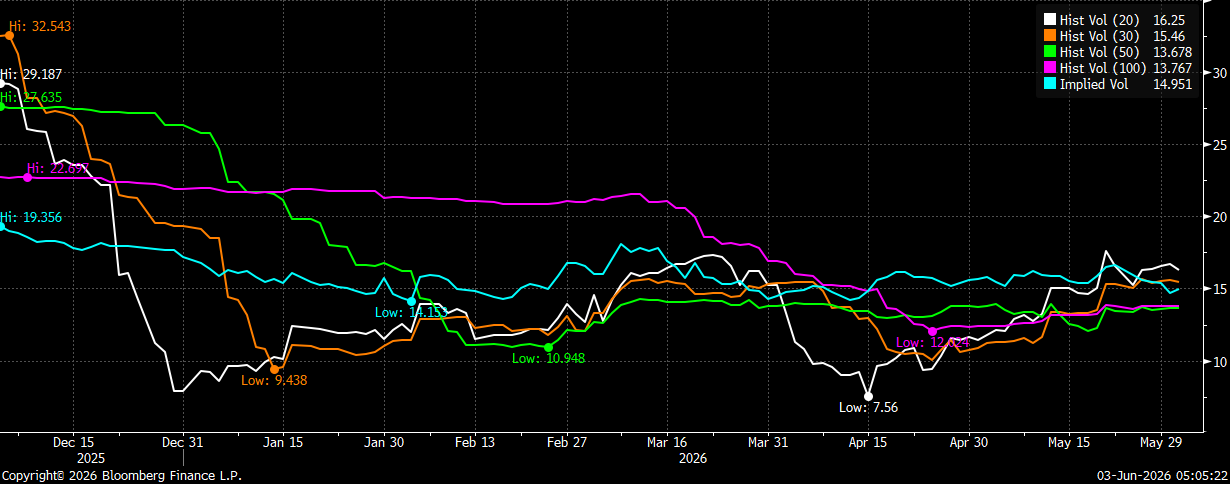

Wheat

Kc wheat

Miax wheat

Oats

Rough rice

Cotton

Canola

Feeder cattle

Live cattle

Lean hogs